请教怎么计算一段日期的累计收益率?

老师好:

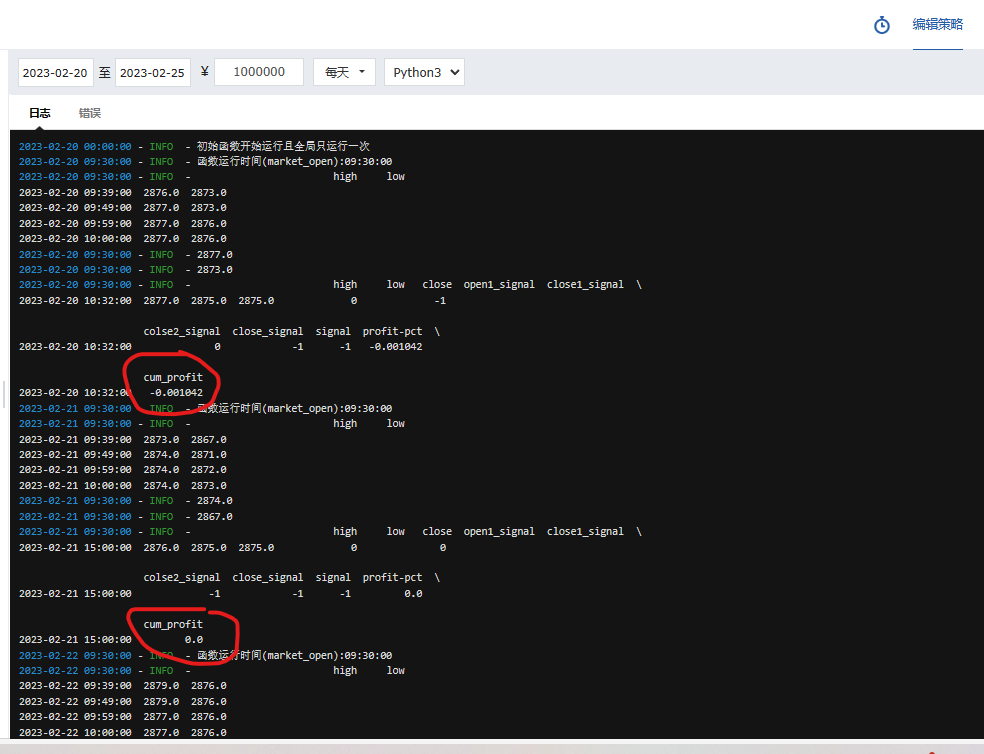

我编了段代码,玉米期货日内交易,即以开盘后30分钟的最高价和最低价为依据,突破最高价开仓买入;当价格小于最高价-(最高价-最低价)/3时止损;当时间到15.00时平仓。代码可以得出当天的收益率,**请教怎么计算一段日期的累计收益率?**代码如下:

# 导入函数库

from jqdata import *

pd.set_option('display.max_columns', None)#显示所有列

## 初始化函数,设定基准等等

def initialize(context):

# 设定沪深300作为基准

set_benchmark('000300.XSHG')

# 开启动态复权模式(真实价格)

set_option('use_real_price', True)

# 过滤掉order系列API产生的比error级别低的log

# log.set_level('order', 'error')

# 输出内容到日志 log.info()

log.info('初始函数开始运行且全局只运行一次')

g.security = 'C9999.XDCE' #玉米合约

# 开盘时运行

run_daily(market_open, time='every_bar', reference_security='000300.XSHG')

# 开盘时运行函数

def market_open(context):

log.info('函数运行时间(market_open):'+str(context.current_dt.time()))

security = g.security

date1=(context.current_dt)#每天开盘时间

date2=(context.current_dt+datetime.timedelta(minutes=30))#开盘后30分钟时间

date3=(context.current_dt+datetime.timedelta(minutes=320))#收盘前10分钟时间

#获取开盘后30分钟的最高H和最低价L

df=get_price(security, start_date=date1, end_date=date2, frequency='10m', fields=['high', 'low'], fq='pre')

print(df)

H=df['high'].max()

L=df['low'].min()

print(H)

print(L)

#获取每天数据(1分钟周期的'high', 'low','close')

df1=get_price(security, start_date=context.current_dt, end_date=(context.current_dt+datetime.timedelta(minutes=330)), frequency='1m', fields=['high', 'low','close'], fq='pre')

df1[ 'open1_signal']=0

df1['close1_signal']=0

df1['colse2_signal']=0

for i in range(len(df1)):

a=df1.index[i]

if date2<a<=date3:

if df1.loc[a,'close']>H:

df1.ix[i, 'open1_signal'] = 1 # 买入开仓信号

elif df1.loc[a,'close']<(H-(H-L)/3):

df1.ix[i, 'close1_signal'] = -1 #卖出平仓信号

elif a==(context.current_dt+datetime.timedelta(minutes=330)):

df1.ix[i, 'colse2_signal'] = -1 #卖出平仓信号

df1['close_signal']=df1['close1_signal']+df1['colse2_signal']

df1['signal']=df1[ 'open1_signal']+df1[ 'close_signal']

#数据清洗,去除['signal']中重复的1,-1

df1.drop_duplicates(subset=['signal'], keep='first', inplace=True)

#-1先于1,属无效信号,将其转换成

df1['signal'] = np.where((df1['signal'] == -1)

& (df1['signal'].shift(-1) == 1), 0, df1['signal'])

#数据清洗,去除['signal']中有0的行

df1 = df1.loc[df1['signal'] * df1['high'] != 0]

#计算当次收益率

df1['profit-pct']=(df1['close']-df1['close'].shift(1))/df1['close'].shift(1)

df1=df1[df1['signal']==-1]

#计算累计收益率(这里只能计算当天的累计收益率)

df1['cum_profit'] = pd.DataFrame(1 + df1['profit-pct']).cumprod() - 1

print(df1)

1131

收起

正在回答 回答被采纳积分+3

1回答

相似问题

复利年华收益率

1024

0

1

和老师计算的结果完全不同

1261

0

4

在计算某项策略的时候,夏普比率计算公式应该怎么用

1104

0

2

看不懂为什么累计收益 = (1 + 当天收益率)的累计乘积 - 1

1317

1

2

关于计算cum_profit的问题

1684

0

1

登录后可查看更多问答,登录/注册