和老师计算的结果完全不同

代码 完全一样,但是计算出结果 完全不同 。。。。居然是亏的

def ma_strategy(data, short_window=5, long_window=20):

""“

双均线策略

:param data: dataframe, 投资标的行情数据(必须包含收盘价)

:param short_window: 短期n日移动平均线,默认5

:param long_window: 长期n日移动平均线,默认20

:return:

”""

data=pd.DataFrame(data)

# 计算技术指标:ma短期、ma长期

data[‘short_ma’] = data[‘close’].rolling(window=short_window).mean()

data[‘long_ma’] = data[‘close’].rolling(window=long_window).mean()

# 生成信号:金叉买入、死叉卖出

data['buy_signal'] = np.where(data['short_ma'] > data['long_ma'], 1, 0)

data['sell_signal'] = np.where(data['short_ma'] < data['long_ma'], -1, 0)

# 过滤信号:st.compose_signal

data = strat.compose_signal(data)

#

# 计算单次收益

data = strat.calculate_prof_pct(data)

# 计算累计收益

data = strat.calculate_cum_prof(data)

# 数据预览

# print(data[['close', 'short_ma', 'long_ma', 'buy_signal', 'sell_signal']])

# 删除多余的columns

data.drop(labels=['buy_signal', 'sell_signal'], axis=1)

#

return data

if name == ‘main’:

# df = st.get_single_price(‘000001.XSHE’, ‘daily’, ‘2020-01-01’, ‘2021-01-01’)

# df=ma_strategy(df)

# # 筛选有信号点

# df = df[df[‘signal’] != 0]

# # 预览数据

# print(“开仓次数:”, int(len(df)/2))

# print(df)

# # print(df[[‘close’, ‘short_ma’, ‘long_ma’, ‘signal’]])

# print(df[[‘close’, ‘signal’, ‘profit_pct’, ‘cum_profit’]])

# # print(data)

# 股票列表

stocks = ['000001.XSHE', '000858.XSHE', '002594.XSHE']

# 存放累计收益率

cum_profits = pd.DataFrame()

# 循环获取数据

for code in stocks:

df = st.get_single_price(code, 'daily', '2016-01-01', '2021-01-01')

df = ma_strategy(df) # 调用双均线策略

cum_profits[code] = df['cum_profit'].reset_index(drop=True) # 存储累计收益率

# 折线图

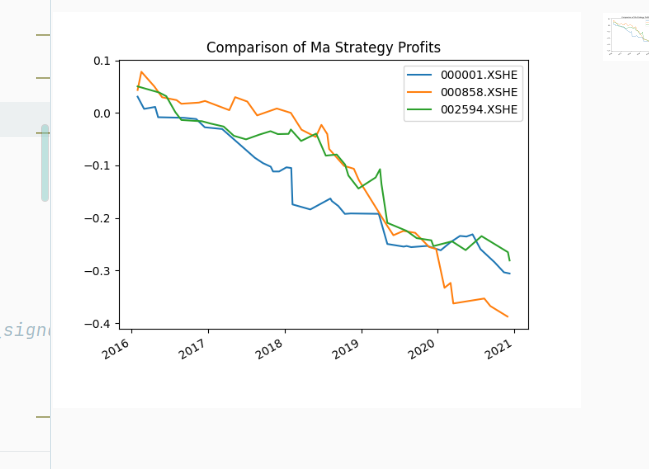

df['cum_profit'].plot(label=code)

# 筛选有信号点

# df = df[df['signal'] != 0]

# 预览数据

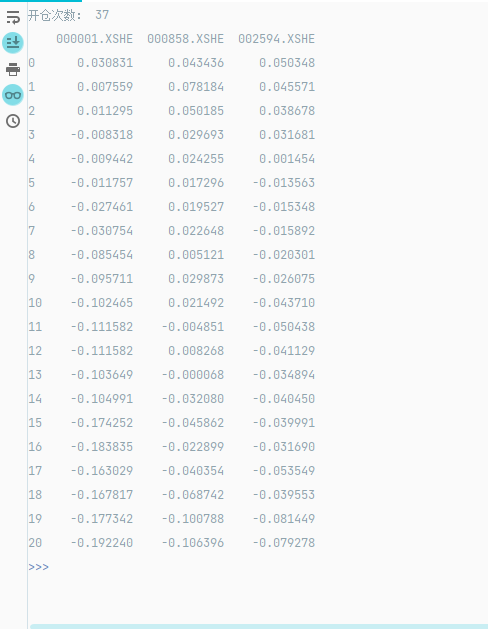

print("开仓次数:", int(len(df)))

# print(df[['close', 'signal', 'pro 、fit_pct', 'cum_profit']])

# 预览

print(cum_profits)

# 可视化

# cum_profits.plot()

plt.legend()

plt.title('Comparison of Ma Strategy Profits')

plt.show()

正在回答 回答被采纳积分+3

3回答

相似问题

登录后可查看更多问答,登录/注册